The SAFE Pile-Up: How Three "Simple" Agreements Became a Dilution Bomb

Millie built a strong product. She had paying customers, a clear wedge into her market, and three investors who believed in her early enough to write checks when nobody else would. Over fourteen months, she raised $750,000 across three SAFEs. Each one felt small. Each one felt reasonable. Each one was a post-money SAFE — the standard YC instrument that 90% of pre-seed founders are signing right now, according to Carta's Q1 2025 data.

Then she got a term sheet.

Her Series A lead offered $3 million at a $12 million post-money valuation. Solid terms for a company at her stage. She ran the mental math in her head: 25% to the new investor, 15% option pool, maybe another 6% or so to the SAFE holders. She figured she'd keep somewhere around 55%.

She kept 40%.

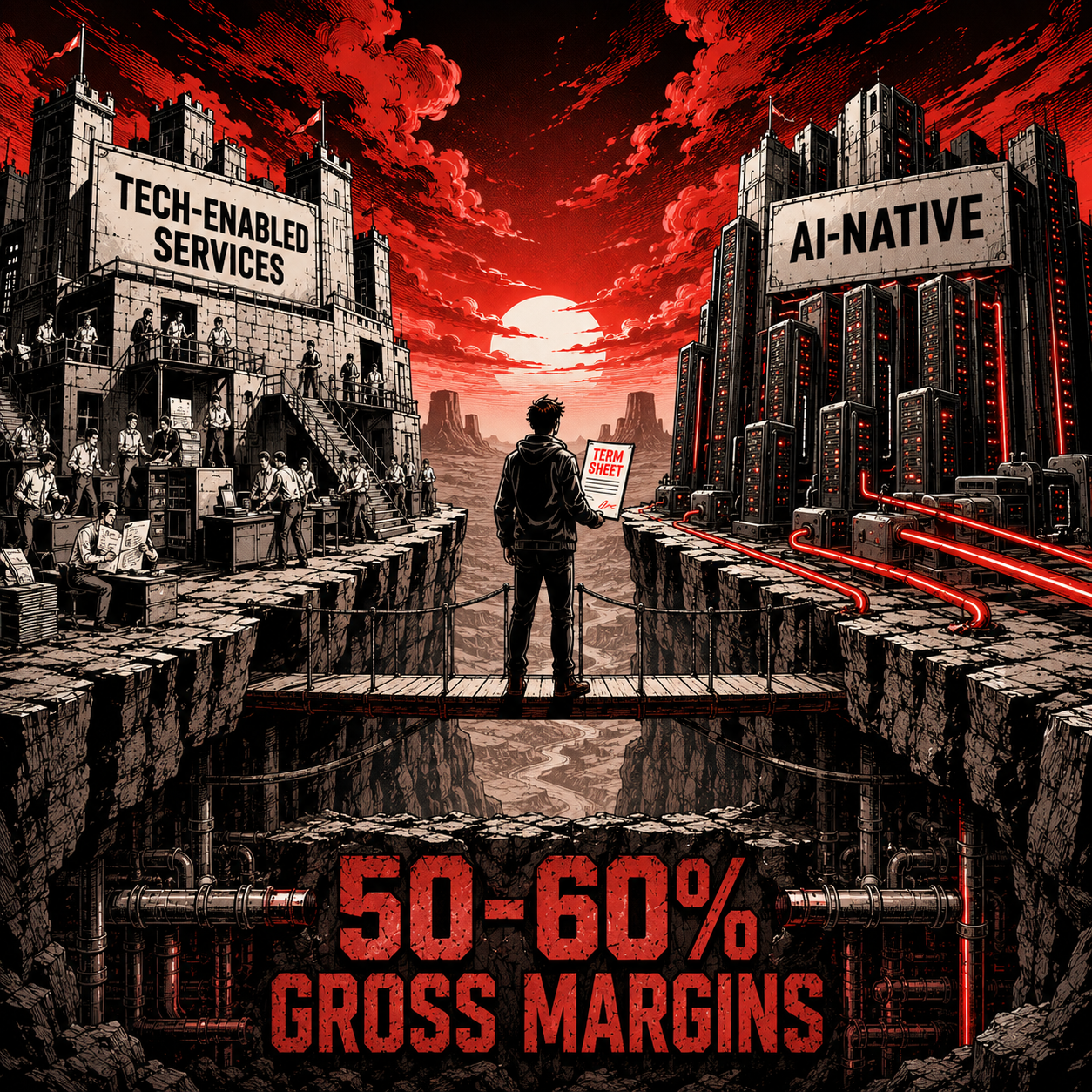

Is AI Software? The $230,000 Question Hiding in Every Revenue Dollar.

There's a comfortable assumption sitting underneath every services-as-software pitch deck. It goes like this: the AI delivers the work, so there are no humans on payroll, so the gross margins should be at least as good as traditional software — maybe better, because you're capturing the full value of a service without the labor cost.

It's wrong. The data showing it's wrong is now public, structural, and getting worse on the timescales most founders are pricing rounds on. If you took anything from Part 1, you should be asking the obvious follow-up: if Sierra and Greenlite both deliver outcomes, why is one priced like software and the other priced like a services firm? The answer, which most founders never get told before they sign a term sheet, is that they actually have similar gross margins. The difference is which one is allowed to claim software multiples in the market right now.

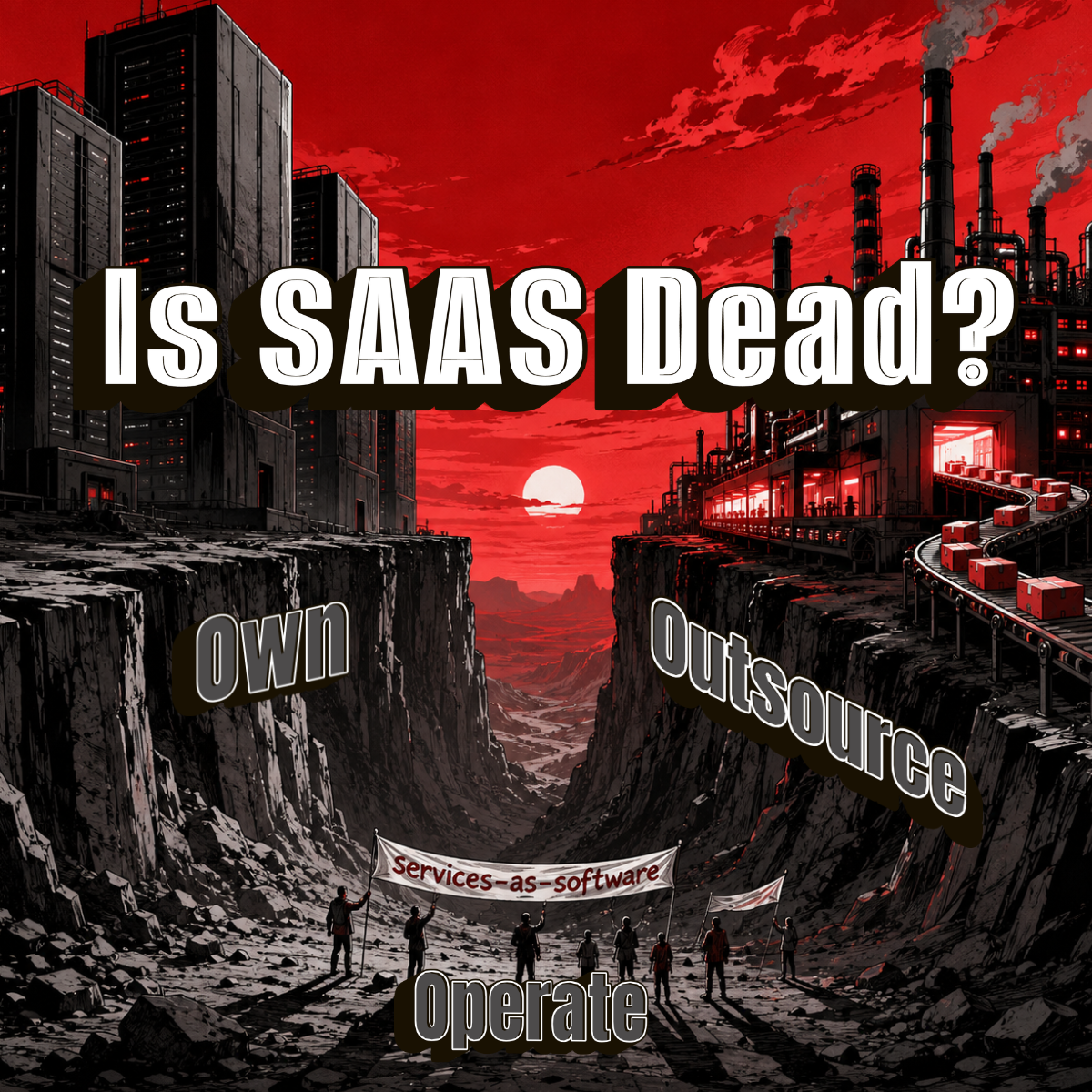

Is SaaS Dead? The $2 Trillion Question Hiding in Every AI Pitch Deck

VCs have repositioned around AI-native companies that don't sell tools — they sell outcomes. Services-as-software (SaS). A new category for a new era, sold to LPs as the answer to the SaaS multiple compression problem.

Here's the problem: most of the companies pitched into that category aren't services-as-software. They're tools dressed up in outcome language.

Here's a founder-grade test that will tell you which side of the line your company is actually on — before a Series B diligence partner does it for you.

The Perfect Storm: Why Venture Capital's Liquidity Crisis Is Reshaping Startup Funding

When Goldman Sachs announced it would acquire Industry Ventures for up to $965 million last week, the deal underscored a seismic shift happening beneath the surface of venture capital: the secondary market has exploded from a niche tool into a $152 billion necessity, fundamentally changing how startups get funded and how investors get paid back.

For better or worse, this is the new reality of startup funding. VCs can no longer afford to simply "spray and pray" and wait for exits. They need active liquidity management strategies. And that fundamentally changes what kinds of companies get funded and how.

Welcome to America, Where You Can Buy a Company—But Not Run It

The Nippon Steel deal may be remembered as a turning point not just for industrial policy, but for how the U.S. is perceived by global investors. In a geopolitical moment defined by economic competition and fragmented alliances, the U.S. must choose: will it lead by example as an open, rules-based economy or slide into the very model of conditional capitalism it has long criticized in others?

The golden share may be strategic. But unless applied with extreme caution, it could prove to be short-sighted, self-defeating, and a poor trade for long-term investment leadership.

What Makes a Healthcare Startup Attractive to VCs and Private Equity?

So far in 2025, Pittsburgh-based healthcare startup Abridge has landed $250 million in funding, UK-based OrganOx closed $142 million, and Transcarent merged with Accolade, Inc.. Both Transcarent and Datavant appear to be open to additional acquisitions as they build toward IPO. Meanwhile, healthcare investors and several healthcare mega-companies have signaled that they "don't much of an appetite" for big deals this year according to Business Insider.

What does this mean? Let's figure this out!