Is SaaS Dead? The $2 Trillion Question Hiding in Every AI Pitch Deck

Part 1 of The Services-as-Software Files.

Is SaaS dead?

The market has spoken: Between January 15 and February 14, 2026, roughly $2 trillion in market capitalization evaporated from the software sector. Atlassian down 35%. Salesforce down 28%. The investor case: AI can rebuild most of these products in months, and the customers who paid SaaS multiples for them for a decade are starting to do exactly that.

So the smart money has moved. VCs have repositioned around AI-native companies that don't sell tools — they sell outcomes. Services-as-software (SaS). A new category for a new era, sold to LPs as the answer to the SaaS multiple compression problem.

Here's the problem: most of the companies pitched into that category aren't services-as-software. They're tools dressed up in outcome language.

Here's a founder-grade test that will tell you which side of the line your company is actually on — before a Series B diligence partner does it for you.

This is Part 1 of a three-part series on the shift from SaaS to SaS: what's actually happening to value in this market, what the economics underneath the marketing actually look like, and what founders should do about it before pricing their next round.

The framework everyone is citing

The broader thesis underneath this — that AI lets software companies eat services markets, and that "selling the work" beats "selling the tools" — was articulated by Sarah Tavel at Benchmark in early 2024 and formalized by Foundation Capital that April. The piece a year later that gave the thesis a clean analytical structure came from Jackie DiMonte at Grid, and it's the framework I want to work with here.

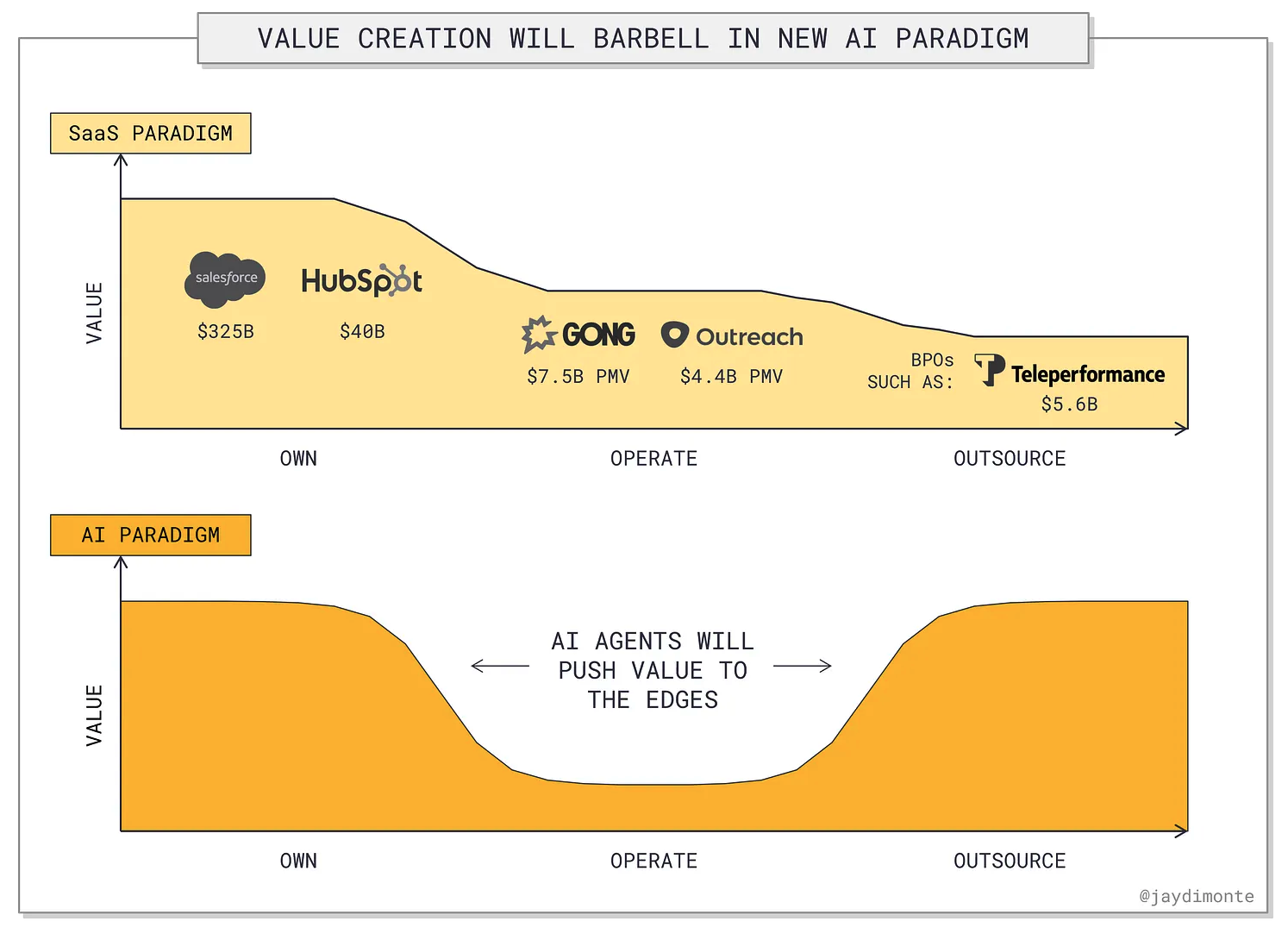

DiMonte's framework asks how the customer chooses to solve a problem: they can own the solution and use a vendor's tools to do the work themselves; they can outsource the work to a party that delivers the finished outcome; or they can sit in the middle and operate alongside the vendor, sharing the responsibility. In software terms, that maps to systems of record like Salesforce or HubSpot (own), specific-function tools like Gong or Outreach that sit beside them (operate), and BPO-style service providers (outsource).

Her observation, borrowed from how mature industries actually distribute value: the money sits at the extremes (own and outsource). The middle gets squeezed. VCs like DiMonte are betting that AI will accelerate the squeeze: the system of record can build the middle's functionality natively, and the service provider can use AI to deliver outcomes more cheaply than ever.

It's a useful framework. It also got stretched into something it shouldn't be almost immediately.

How the category got laundered

The implied multiple for a services-as-software company in 2026 has climbed to roughly 50-100x revenue, while traditional SaaS is collapsing toward 5-10x. That spread is what's driving valuations like Sierra at $10B+, Decagon north of $4B, Harvey at $11B, and EvenUp at $2B+. The reward for landing on the right side of that line is roughly a 10x valuation difference.

So every founder building a vertical AI product has been told — sometimes explicitly by their investors — to position the company as services-as-software. The deck gets rewritten. The pricing page gets a revenue-share tier. The marketing language pivots from "tool" to "outcomes." The agent architecture gets relabeled "agentic." A multi-agent orchestrator with task-specific sub-agents gets described as a "compound vertical AI platform," which is a phrase that means nothing and is now in roughly half of the legal and healthcare AI pitch decks I see.

None of this changes the underlying business. It just changes what the business looks like in a deck.

The test that cuts through

Here is the question that sorts this out in about thirty seconds:

Who produces the deliverable the paying customer actually uses?

Not who builds the tool. Not who runs the workflow. Not who gets credit on the marketing site. Who is legally and operationally responsible for the artifact or outcome that the customer is hiring you to provide?

Run a few real companies through it.

Greenlite delivers construction permits. They acquired licensed plan reviewers as employees. They submit the plans to the building department. The municipality issues the permit to Greenlite, who hands it to Walgreens or O'Reilly Auto Parts. The deliverable — a stamped, approved permit — is produced and delivered by Greenlite. ✅ Outsource.

Sierra runs customer service. The end consumer interacts with Sierra's agent. The refund either gets issued or it doesn't. The interaction is completed (or escalated) by Sierra. The enterprise customer pays for a resolved ticket as the deliverable. ✅ Outsource.

Harvey is legal AI. A lawyer logs in, runs a query, gets a memo or redline back, reads it, edits it, signs it under their bar number, and sends it. The deliverable that the law firm's client receives is signed and produced by the lawyer. Harvey helped them produce it faster. ❌ Operate.

EvenUp is personal injury AI — and they market hard as services-as-software, with positioning like "Pre-Litigation as a Service" and "$10 billion in settlements." Look at what actually happens: the PI attorney loads case data, EvenUp drafts a demand letter and builds a medical chronology, the attorney reviews, edits, signs, and sends. The insurance carrier corresponds with the law firm. The injured plaintiff is represented by the lawyer. The $10B in settlements were won by lawyers using EvenUp, not by EvenUp. ❌ Operate.

Notice the pattern. Where the vertical has a licensing requirement — law, medicine, accounting, financial advice — there is structurally a licensed human in the producer-of-record seat. You can't remove them without either (a) absorbing the license yourself by employing the credentialed humans, or (b) breaking the law.

Greenlite chose (a). Most AI legal and healthcare startups have not. Which makes them operate-tier, no matter how the deck is written.

What's actually happening

Two things are true at the same time, and you need to hold both.

The phenomenon is real. AI is making tech-enabled services economical at scales that pre-AI agencies and BPOs couldn't reach. Some companies — Sierra, Decagon, Greenlite, Pilot.com, Mercor, Lovable, Cognition — are genuinely delivering outcomes. They tend to live in verticals without licensing barriers, or they absorbed the licensure by hiring the credentialed humans directly. The economics are different from traditional SaaS. The multiples are warranted, at least for the companies that actually fit.

The category has been stretched to roughly ten times its real footprint. Most "services-as-software" companies in 2026 are operate-tier startups using outcome-flavored language to escape SaaS multiple compression. The marketing layer has been laundered through investor decks, partnership announcements, and conference panels until "agent" stopped meaning anything specific and "outcomes" stopped meaning a deliverable the AI company actually produces.

The reckoning won't be that services-as-software turns out to be fake. It'll be that the genuine category was maybe a tenth the size of what got funded under the label. The Sierra-tier winners will look extraordinary in retrospect. Everyone else will quietly reprice down to whatever their actual business model justifies — which is, in most cases, a perfectly respectable operate-tier company with operate-tier multiples.

What this means if you're building

A few practical takeaways if you're a founder running into the language right now.

The test isn't what you call yourself. It's what you deliver. If your customer is a licensed professional and you're producing artifacts they review, edit, and sign — you are an operate-tier company. Calling yourself services-as-software does not change this. It changes how disappointed your investors will be when they figure it out, which they will, usually at the worst possible moment in your next raise.

Operate-tier is not a death sentence. Pretending you're not one is. Some of the largest AI companies by revenue right now — Cursor, GitHub Copilot, Gong, Outreach — are operate-tier. They're growing fast. They have real moats: distribution, workflow embedding, data flywheels, deep integrations into systems of record. What kills operate-tier companies isn't being operate-tier. It's getting funded on outsource expectations and then missing them.

There are exactly three real escape paths from the ditch.

The first is to become a system of record yourself. Make your product the place the work happens, not the place that helps the work happen. This is the path Harvey is trying to walk into with Microsoft 365 integration, the Lexis partnership, and embedded legal engineering teams inside customer firms. It is expensive and slow and requires distribution at a scale most startups will never reach.

The second is to absorb the licensure. Hire the credentialed professionals and become the service provider. This is the Greenlite path. It changes your unit economics, your hiring profile, your insurance, and your regulatory footprint. You are no longer a software company; you are a tech-enabled services company. Some VCs still want to fund this. Some don't.

The third is to find a vertical without a licensing wall. Customer service. App building. Talent sourcing. Translation. Light construction permitting. This is the path of least resistance and the path where the genuine services-as-software multiples make sense.

Price your round on what you are, not what you're called. If you raise an outsource-tier round on an operate-tier business, your next round resets to operate-tier metrics, and you spend the in-between cleaning up a cap table that doesn't match the company you actually built. Founders lose far more equity to multiple compression on a down round than they lose to taking a sober up round earlier. I see this play out the same way every cycle: the up-round euphoria looks great on the day it closes and looks expensive at every subsequent decision point.

The honest read

Services-as-software is a real shift. It's also a marketing label that has been applied to ten times the number of companies it actually describes, because VCs paying outsource multiples are happy to be told they're funding outsource companies, and founders pricing rounds on those multiples are happy to oblige.

The cleanest founder framing I can offer: if your vertical has licensing rules that force a credentialed professional into the producer-of-record seat, you cannot be services-as-software without becoming the licensed provider. You can build a great operate-tier company, and you can plausibly graduate to a system of record, but the outsource path is closed unless your company itself absorbs the credential.

That's a real strategic choice. It deserves more than a slide in the deck.

Getting your positioning right before you raise is the difference between a clean Series A and a down round you spend the next eighteen months explaining. The Investor Readiness Vault™ is built for exactly this — getting your structural story straight, your diligence file clean, and your category positioning defensible before a partner asks the question. Most founders book this two raises too late. Book a 20-minute call

Part 2 of The Services-as-Software Files lands in two weeks: a deep dive into the margin and exit-multiple economics underneath services-as-software — and why "fewer humans" doesn't actually mean "higher margins." Part 3 follows with a methodology piece on how to stress-test a VC thesis without falling for the deck.

#VentureCapital #AIStartups #ServicesAsSoftware #FounderAdvice #Defensibility #InvestorReady #LegalForFounders